Most people picture a real estate attorney as someone who shows up at the closing table, watches you sign a stack of papers, and collects a check. That picture is wrong, and the gap between that assumption and reality can cost you thousands of dollars or derail your transaction entirely. The role of real estate attorney home closing involves far more than witnessing signatures. From title searches and document preparation to fund disbursement and fraud prevention, attorneys serve as the legal backbone of one of the largest financial transactions most people ever make.

Table of Contents

Key takeaways

|

Point |

Details |

|---|---|

|

Attorney states have strict rules |

22 states plus DC require a licensed attorney to perform key closing tasks by law. |

|

Attorneys do more than paperwork |

Real estate attorney duties include title searches, lender coordination, document preparation, and fund disbursement. |

|

Title companies have legal limits |

Title companies handle administrative tasks but cannot give legal advice or resolve complex title defects. |

|

Early engagement saves money |

Hiring an attorney at the contract stage catches risks before they become expensive disputes. |

|

Wire fraud is a real threat |

Always verify wire transfer instructions by phone. Email-only instructions are a major red flag. |

Role of real estate attorney in home closing: state requirements

Not every state gives attorneys the same authority in a real estate transaction. 22 states plus DC require attorney involvement in home closings by law or bar opinion. States like Georgia, Massachusetts, New York, South Carolina, and West Virginia fall into this category. In these jurisdictions, only a licensed attorney may prepare deeds, conduct title reviews, and perform other legally defined closing tasks.

In the remaining states, title companies or escrow officers typically manage the closing process. These are often called “escrow states” or “title states,” and they operate quite differently from attorney-closing states.

|

Feature |

Attorney-closing states |

Escrow/title states |

|---|---|---|

|

Who conducts closing |

Licensed attorney |

Title company or escrow officer |

|

Legal advice available |

Yes |

No |

|

Title opinion provided |

Yes |

No (title insurance only) |

|

Fund management |

Attorney IOLTA account |

Escrow account |

|

Deed preparation |

Attorney required |

Title company or agent |

One detail that surprises many buyers and sellers is how attorneys manage money. In attorney-closing states, attorneys hold funds in IOLTA accounts acting as fiduciaries for the transaction. IOLTA stands for Interest on Lawyers’ Trust Accounts. This structure means the attorney is legally responsible for every dollar that passes through the closing, from the buyer’s down payment to the seller’s net proceeds. That fiduciary obligation is not something a title company or escrow officer carries in the same legal sense.

The practical implication is significant. When an attorney controls the funds and records the deed, there is a licensed professional with a legal license on the line who is accountable for the outcome. That accountability changes the nature of the closing entirely.

What a real estate attorney actually does at closing

The home closing attorney role covers a broad range of tasks, and most of the work happens well before you sit down at the closing table.

-

Title search and examination. Attorneys conduct thorough title searches to uncover liens, easements, unpaid taxes, or ownership defects that could cloud the title. This is not just a database lookup. It requires legal interpretation of what those findings mean for your transaction.

-

Document preparation and review. Primary responsibilities include document preparation such as deeds, purchase agreements, affidavits, and transfer documents. Attorneys also review every document for legal accuracy before you sign.

-

Lender coordination. In financed transactions, attorneys act as the final legal checkpoint for compliance with state and federal laws including RESPA (the Real Estate Settlement Procedures Act). They follow written lender instructions precisely, and any deviation can create liability.

-

Closing meeting facilitation. The attorney manages the actual closing meeting, guiding all parties through document signing, answering legal questions on the spot, and coordinating the exchange of funds.

-

Post-closing recording and disbursement. After signatures are collected, the attorney records the deed with the county, then disburses funds to all parties. Sellers typically receive net proceeds within 24 to 48 hours after closing.

One nuance that catches buyers off guard involves who the attorney actually represents. Closing attorneys often represent the lender in financed transactions and must follow lender instructions above all else. They can act neutrally for the buyer and seller as long as no conflict arises, but their primary legal obligation runs to the lender. This does not mean they are working against you. It means you should understand whose interests are formally protected.

Understanding the documents you sign is another underappreciated part of the attorney’s job. The Closing Disclosure and ALTA Settlement Statement serve different legal and accounting purposes, and confusion between them can delay closings. The Closing Disclosure explains your loan terms. The ALTA Settlement Statement reconciles every financial aspect of the transaction. An attorney who explains both clearly prevents last-minute surprises.

Pro Tip: Ask your attorney to walk you through the ALTA Settlement Statement at least 48 hours before closing. Reviewing it in advance gives you time to catch errors without the pressure of a closing deadline.

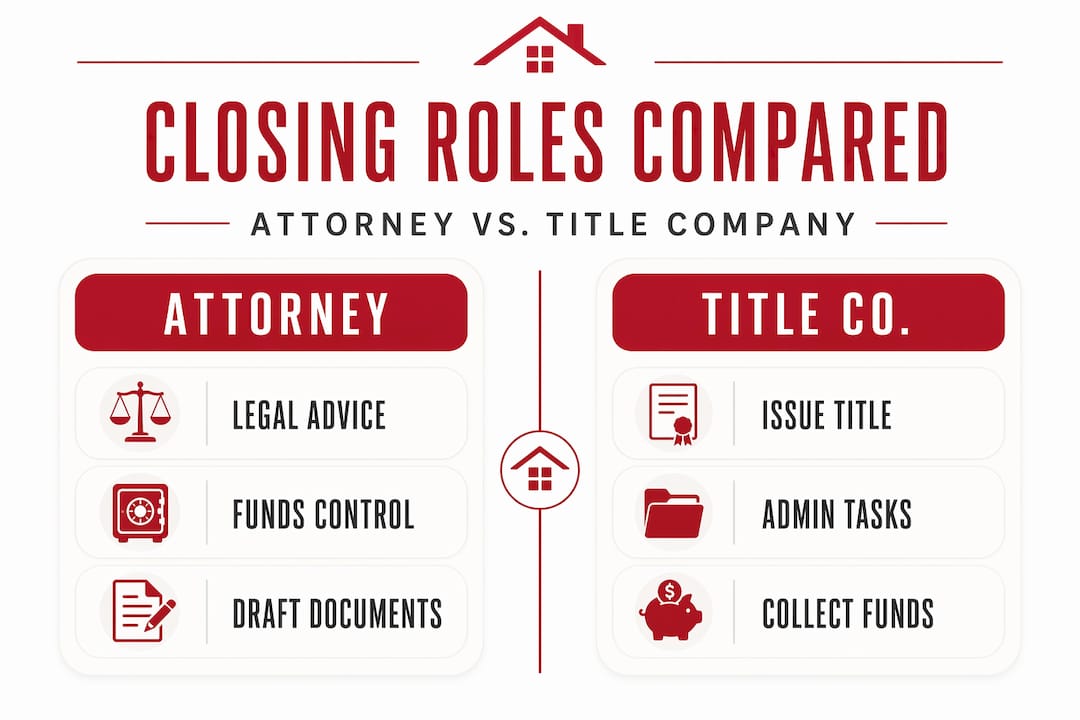

Attorneys vs. title companies vs. escrow officers

The importance of real estate lawyers becomes clearest when you compare what they can do versus what title companies and escrow officers are legally permitted to do.

Title companies are licensed to conduct administrative closing tasks. They issue title insurance, collect and distribute funds, and prepare standard closing documents in states that allow it. What they cannot do is provide legal advice, interpret contract language for you, or resolve a complex title defect. Title companies lack legal authority to give legal counsel, which means if a problem surfaces during the title search, they can flag it but cannot advise you on how to handle it legally.

Escrow officers function as neutral administrators. They hold funds, collect documents, and follow instructions from both parties. Their role is procedural, not legal. In a straightforward transaction with no complications, that may be sufficient. But real estate transactions rarely stay simple.

Here is where attorney involvement in home closing becomes genuinely protective:

-

When a title search reveals an old lien from a previous owner, an attorney can draft a release and negotiate its resolution. A title company cannot.

-

When contract language is ambiguous about who pays a specific closing cost, an attorney can provide a legal opinion. An escrow officer cannot.

-

When a dispute arises between buyer and seller over inspection repairs, an attorney can advise on legal remedies. Neither a title company nor an escrow officer can step into that role.

The bottom line is that attorneys offer legal services including title defect resolution and contract legality that no other closing professional is authorized to provide. In complex deals, that distinction is not minor. It is the difference between a transaction that closes cleanly and one that stalls in litigation.

Practical steps for buyers and sellers

Knowing what does a real estate attorney do is one thing. Knowing when and how to engage one is where most buyers and sellers fall short.

-

Hire at the contract stage, not at closing. Early engagement helps detect contract risks before they become expensive disputes. An attorney reviewing a purchase agreement before you sign it can identify unfavorable contingency language, unclear repair obligations, or title issues that would have blindsided you weeks later.

-

Understand the fee structure upfront. Attorneys typically charge flat fees around $1,000 for simple residential transactions. Fees increase with complexity, such as commercial deals, title defects, or contested closings. Get a written fee agreement before work begins.

-

Request your settlement statement early. Settlement statements are typically provided three to five days before closing. Review them carefully and ask your attorney to explain any line item that is unclear.

-

Verify wire instructions by phone, every time. Wire fraud prevention requires phone verification of transfer instructions. Never wire money based solely on email instructions, even if the email looks legitimate. Call the attorney’s office using a number you independently verified, not one provided in the email.

-

Hire your own attorney when conflicts arise. If you sense that the closing attorney’s loyalties are primarily with the lender or another party, retain separate counsel. The cost is modest compared to the risk of proceeding without independent legal advice.

Pro Tip: If you are buying in a state that does not require an attorney, you can still hire one independently. In transactions involving unusual title history, estate sales, or foreclosures, independent legal counsel is worth every dollar.

The San Diego home buying guide from Stuharveyestates walks through the best stages to bring an attorney into your transaction, which is a resource worth bookmarking if you are purchasing in California.

My take on attorneys and the closing process

I have worked alongside real estate attorneys on hundreds of transactions across Southern California, and the pattern I see most often is this: buyers and sellers underestimate the attorney’s role until something goes wrong.

The most common misconception I encounter is that the closing attorney is “on your side” in a financed deal. In my experience, that is not quite accurate. The attorney’s primary obligation in most financed transactions runs to the lender. That does not make them your adversary, but it does mean you should not assume they are advocating for your best interests the way your own counsel would.

What I have learned from watching deals succeed and fall apart is that early legal involvement almost always pays off. I have seen transactions where a title search revealed an unresolved lien from a contractor job done fifteen years prior. The buyer who had an attorney already in their corner resolved it in a week. The buyer who waited until closing scrambled for three weeks and nearly lost the deal.

Choosing an attorney who knows your local market matters as much as their general competence. Real estate law varies significantly by county and municipality, and an attorney who regularly closes deals in your area will catch nuances that a generalist might miss. I always recommend that clients ask prospective attorneys how many transactions they close per month in the specific area where they are buying or selling.

The other thing I tell every client is this: communicate proactively with your attorney. Do not wait for them to call you. Ask questions early, flag concerns the moment they arise, and make sure you understand every document before you sign it. The attorneys who produce the best outcomes are the ones whose clients treat them as partners, not just service providers.

— Stu

Work with a team that knows the closing process

At Stuharveyestates, we have guided buyers and sellers through more than 250 luxury transactions across La Jolla, Rancho Santa Fe, and greater San Diego. Part of that experience is knowing exactly when and how to bring the right legal professionals into your transaction.

We connect our clients with experienced real estate attorneys who understand Southern California’s specific closing requirements, title nuances, and local market conditions. Whether you are purchasing your first property or selling a high-value estate, having the right legal coordination from day one protects your investment and keeps your timeline on track. Browse our current San Diego property listings or explore our buyer support resources to start your search with confidence and the right team behind you.

FAQ

What does a real estate attorney do at closing?

A real estate attorney conducts the title search, prepares and reviews all closing documents, coordinates with the lender, manages the closing meeting, and handles post-closing recording and fund disbursement. Their role is the legal checkpoint that protects all parties and satisfies state and federal compliance requirements.

Which states require an attorney for home closings?

22 states plus Washington DC require attorney involvement in home closings by law or bar opinion, including Georgia, Massachusetts, New York, South Carolina, and West Virginia. In these states, only a licensed attorney may perform key closing tasks such as deed preparation and title review.

Can a title company replace a real estate attorney?

No. Title companies handle administrative closing tasks but cannot provide legal advice, draft legal opinions, or resolve complex title defects. An attorney offers legal authority that title companies are not licensed to provide, making them essential in complicated transactions or attorney-required states.

How much does a real estate closing attorney cost?

Fees for a real estate closing attorney typically start around $1,000 for straightforward residential transactions, with costs rising based on complexity, state requirements, and any title issues that need legal resolution. Always request a written fee agreement before the attorney begins work.

How do I protect myself from wire fraud at closing?

Always verify wire transfer instructions by calling your attorney’s office directly using a phone number you have independently confirmed. Never rely solely on email instructions for wiring money, as email accounts involved in real estate transactions are frequent targets for fraud.